Aligning Incentives in Governance

Intro

This article proposes a solution for increasing voter participation. It does not discuss issues around voter value, proposal value, and governance reputation. Instead, it is a proposed solution, simplified as much as possible, to generate consistent engagement from token holders in governance which is a difficult problem found in all democratic systems.

Having seen a large number of governance tokens in crypto be implemented, as if to represent value and “utility” of a token, there is a distinct disassociation with utility of the governance token and true value of the network.

The value proposition of a governance token is that it acts as a social layer of network security. In general proof of stake, the manipulation of an ecosystem’s current state (ie, attacking consensus) is prevented by the number of staked tokens across a large number of validators.

In a governance token’s case, the governance token protects against attacks on changes to the ecosystem both social and infrastructural.

However, the culture of investors purchasing governance tokens is that investors purchase a token as if it is a representation of the value of the network rather than being a token of security. This has led to astronomical valuations in the billions for governance tokens.

Simply said, fear of SEC regulation aside, investors are treating the governance utility token as if it were a share of a stock–except in crypto’s case, as a share of the network.

This is entirely false, though. A token to protect the network is not a direct 1:1 value of the network itself.

This is further evidenced by the general low participation across the board in governance initiatives. If the token’s value is to be able to vote, and people bought it because they were convinced it was amazing to be able to vote, then wouldn’t people be scrambling to vote any chance they could?

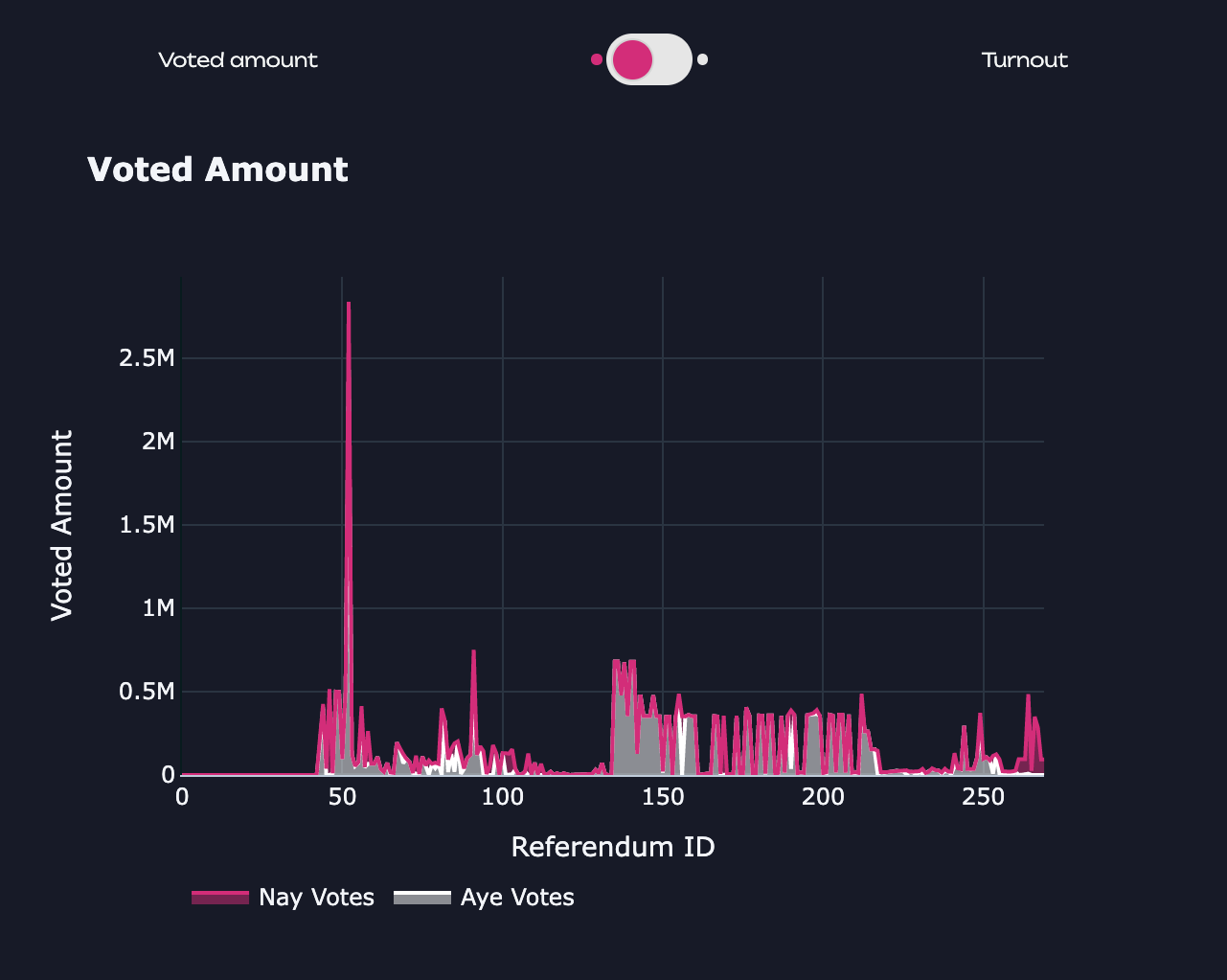

Subjectively, I’ve seen voter turnout in blockchain amounting to 0-7% as “normal”, and voting turnout of 15% of circulating tokens would be a phenomenal feat for a large network. Here’s some data shared by Rich from Decent partners around Decred managing an astonishingly high voter turnout.

This article highlights the reason for high voter turnout:

Firstly, it is important to note that all three of these protocols actively ‘identify’ as self-governing blockchains. It could be that this element of the projects is one of the key draws which appealed to many of the token-holders.

Additionally, and perhaps a greater factor, is that Decred, Cosmos, and Tezos, all provide voters with direct incentives to participate via Proof-of-Stake. So the assumption that token holders will participate in on-chain governance votes purely through their passive ownership seems flawed.

In Kusama governance we see a high of around 9%, and a norm of about half as much.

Regardless, in most all crypto governance, a small number of voters who are essentially the whales of the ecosystem, often just the top 10, and almost always the top 100, can determine everything.

Polkadot and Kusama are arguably no different in terms of whale influence.

In simple terms, this means that 10-100 individuals can decide the fate of all participants numbering tens of thousands to hundreds of thousands of individuals who simply are not incentivized to participate in governance. According to Chainanalysis for major DAOs, 1% of token holders hold 90% of voting power.

TLDR; unless governance tokens are used to secure the future of the network, the governance token has no value.

In my opinion:

governance tokens != network value

And

Voter turnout = governance token value

It is a common thing in crypto to have airdrops of governance tokens. This is so that the voter pool is wide, and there is, in theory, better security with more decentralization.

However, as mentioned, because of low voter turnout, decentralization becomes a myth. This is why there is the emergence of delegation models where those with more knowledge and motive are given the right to vote on the behalf of individuals who trust them.

This is effective in many ways, but the core problem remains that there is still more centralization than decentralization over time, and too much centralization results in social security risks to the entire ecosystem whereby these delegated groups or individuals always vote in their own best interest, very similar to flawed democratic models today.

Worse yet is when the democracy isn’t executed on-chain, still controlled by a single party which is more than not, the actual situation. Even in a multi-sig situation, governance may not be executed except by a small group of individuals.

A recent event highlights this issue, in the highly regarded Arbitrum Airdrop where despite a failing vote, the team issued a statement saying that it was a formality, and not a true vote.

Since, there has been a response to the accusations, but the point remains that a decentralized token in itself does not, even with voter participation, result in decentralization.

Thankfully, we’ve begun exploring Open Gov on Kusama, and eventually Polkadot, where governance decisions are executed on chain automatically.

The simple solution

It’s my opinion that network value needs to approach governance token value for governance token models to be valid.

Though impossible, we should seek to move towards:

Network value = Governance token value

This means that instead of distributing all of a governance token to token holders, the tokens reserved for governance should be given to those that govern.

Before you react and point out the obvious flaw, hear me out.

The problem with paying people to vote are numerous, but perhaps chief amongst them on the grounds of tokenomics is that you are encouraging manipulation and further centralization, and you are inflating the supply.

On the problem of manipulation

Manipulation can be seen in all incentive models, even in Proof of Chaos’ governance NFTs run on Kusama in 2022. The NFTs inherently had no value, but collectors decided to create a market for them and value them accordingly, even so.

Manipulation to earn NFT rewards became common, but at the same time you cannot deny the effectiveness in increasing engagement.

Many lessons were learned through the trial of governance NFTs.

What’s already clear is that not everyone cares about NFTs.

But, it can be self-evident that network participants do care about token incentives, though.

We can prove this by looking at pure staking incentives where active stakers amount to 47% of the network tokens, often approaching 70% in many (even large) networks.

This is because in general staking, there is an alignment of motives where individual greed, altruism, and network security all achieve the same goal. (And of course, it’s generally simpler, and a single action taken which improves participation over time).

Our solution, then, is to do the same for Governance.

The evidence of the efficacy of aligned incentives as seen in Decred, Cosmos, and Tezos models is clear.

While I have only casually fleshed this idea out, I believe that its fundamentals could be the solution.

On the problem of inflating the supply

When rewarding participants who are incentivized not only to vote, but to manipulate, the architecture of the incentives must be carefully considered.

While this is only lightly considered at this stage, here are some thoughts I have. To start, a few premises that are known, but should be established:

- Inflating supply is always a concern for token holders. Too high inflation results in a supply-demand cycle that leads to lower price which affects token holder confidence and overall participation. Thus, inflation rate cannot be increased further, and ideally, should decrease the total supply over time while incentivizing participants.

- Consolidation of tokens to larger holders must be carefully considered whereby those with the most tokens are already incentivized to participate, and those with less tokens are naturally less incentivized.

- Voting alone is not valuable in itself. Referendums in itself do not necessarily offer improvements to the ecosystem. There must be some method to reward only valuable changes to the ecosystem and incentives should align with this.

- Reporting and accountability must align with incentives, especially for ongoing projects, and there must always be a reasonable fail safe that protects token holders from being locked into prior decisions.

- Even without inflation, “personal inflation” or rather an individual’s wallet receiving “free tokens” will result in selling pressure. Incentivizing people to continue participating in governance must recognize the danger of this in human nature.

Initial Ideas with all the above in consideration

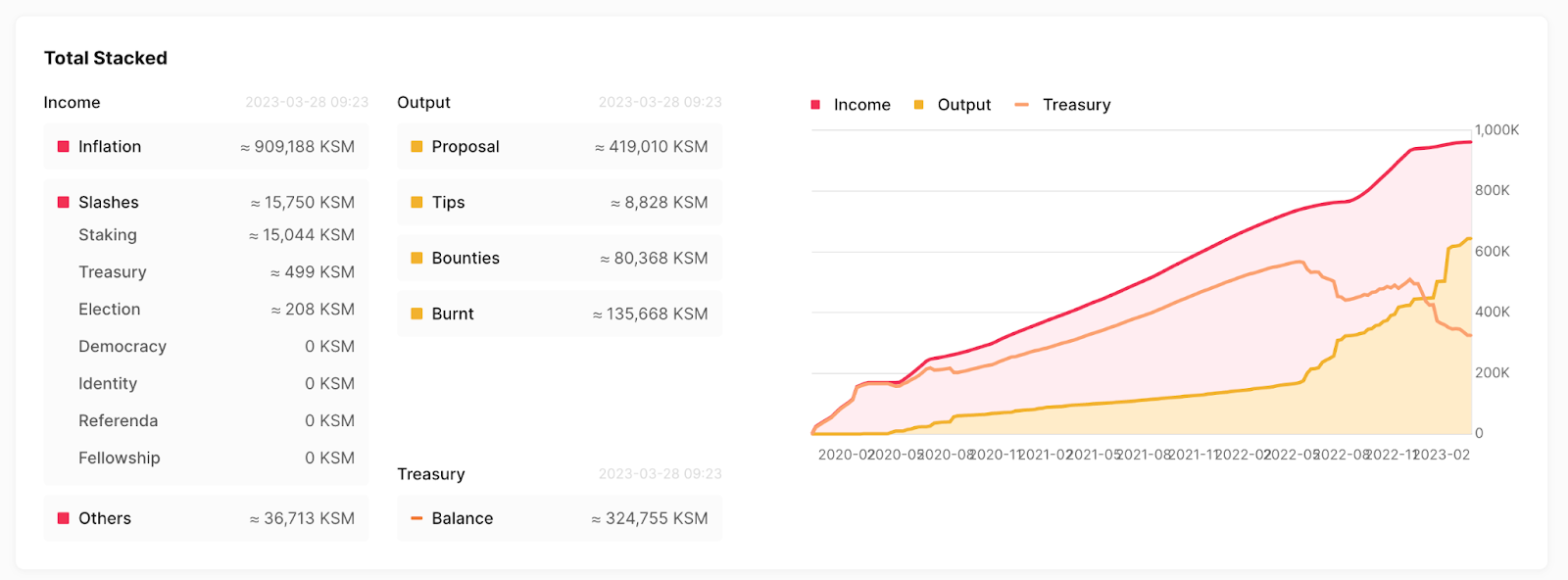

Allocate a portion of treasury for rewards

A significant portion of the treasury, including a portion of future inflation, should be set aside to reward voters in general proportion to the number of tokens held. For every vote that is passed (to help ensure that only valuable proposals are rewarded), token holders will receive a small % of their token back in return as rewards.

Also “total stacked?” “Staked”, you mean?

This % will decrease based on the number of tokens held, because as mentioned, those with large token holdings already are incentivized to participate. However, importantly, the % decrease should not be so significant as to encourage wallet splitting manipulation. It is meant to be a light measure to encourage smaller holder participation but “not be worth the effort” of managing multiple wallets (or bots).

Build a Flywheel Model of Governance

As mentioned, individuals who receive “free tokens” are likely to dump. In what can only be seen as one of the strongest flywheel models in crypto thus far, GMX is a perpetuals exchange that has achieved incredible volume and TVL to support their perpetuals, while being one of the only protocol DeFi tokens to 10x during the bear market because of its flywheel model and clear utility.

Countless DeFi models have emerged directly emulating GMX’s flywheel model.

For those unfamiliar with flywheel models, it’s the idea that there should be incentives to return tokens to a locked state so that protocol rewards don’t dilute the supply, and cause downward price action, protecting investors.

We’ve seen failed models with poor flywheels in most all DeFi protocols aside from models like GMX where tokens are given fully unlocked to participants, and yet they are unable to gain TVL without these incentives.

We thankfully have freedom in governance to circumvent issue because participants already hold tokens and are already invested in the protocol.

However, we still cannot neglect the need for an ideal flywheel design.

On the other hand, some governance models have attempted to make flywheels too restrictive, resulting in individuals not participating because token restrictions are so aggressive that there seems to be no point in participating at all.

Using GMX as inspiration and combining it with existing conviction models already available, I would propose a model in parallel to the current conviction weighting system.

Those who are willing to add their rewards as a separate parallel “conviction” model can lock up their rewards and multiply the value of their tokens during governance rather than collecting their reward immediately.

This means that those who participate the most, over time, will end up with more tokens to add to their “conviction” and thus, reward weight. They can choose to withdraw their tokens at any time, but there will be an immediate modification of the “conviction” they’ve accumulated to reflect how much they’ve withdrawn in rewards.

In the situation that an individual adds more tokens to their voting power, this will also naturally reduce their parallel conviction reward multiplier because it must correlate to how many tokens they are voting with.

Delegation Reward Reduction

As mentioned, delegation to known experts results in higher centralization and often self-serving manipulation. I would first suggest that those voting with delegated tokens would split the voting rewards between delegators and themselves, and have a reduction of overall rewards by 20% between the two parties.

Return Delegation

Additionally, I would suggest a “return delegation” model where those who hold a high amount of delegated tokens are naturally given a lesser % reward (again, without being too aggressive as to reduce participation).

To prevent this reward from depreciating too much, however, there is another incentive.

They can “return delegate”, or allocate their voting power to different individuals/parties who may be better informed than they are.

This will be categorical, in which they can choose types of spends, categories of spends, or topics, and have these certain parties or individuals vote on their behalf with the total tokens that have been delegated to them.

It could work in tandem with agile delegation which allows delegation to specific experts, but it could go even further in that more delegations to further sub or sub-sub-topics could be better rewarded.

This of course has other manipulation risks (as in simply delegating to different self-owned wallets), but if return delegations are only available to those with an x month history and on-chain identity, it could help prevent such manipulation.

By decreasing rewards to those who do not return delegate, it leads to a distribution of responsibility in a way that furthers decentralization, while preserving the value proposition of original delegation.

Token Burning

Perhaps the most controversial aspect to this ideation is the consideration of token burning. Right now, we are utilizing more of a treasury that has been ultimately under-utilized on DOT, and recently over-utilizing the treasury in KSM. Asking to increase the circulating supply no matter what, even with a strong flywheel design, will lead to additional selling pressure.

I would propose the possibility that for every successful proposal passed that achieves a voter threshold (such as 15%), that an equivalent portion of tokens requested by the passed proposal is burned from the treasury.

The reasons are this:

- It would encourage overall careful spending of the treasury.

- It would help counter the general long-term consequences of an increasing circulating supply.

- It would counter-intuitively protect from the additional spending when voter turnout, being incentivized, becomes so large that rewards are extremely high.

- It answers the question of “who pays for the burn?” Token holders won’t be okay with countering an inflating supply with their own tokens, nor will validators agree to decreasing supply. So, who else could take on the burden of this spend but the treasury itself, and increasing circulating supply is a major issue, always.

This is merely the first draft of this document, spun up train-of-thought, but I hope it provides some ideas to consider as we are facing challenging issues around Open Gov.

The federal government spent an estimated $340 million in voter education and outreach in 2020, but including state education, 1.2 billion was spent to achieve around 50% participation in election voting.

Thus, I believe that with this model, the active participation and the encouragement of frugality would pay for itself in the long-term. I look forward to hearing your thoughts.

Pnin

If you found value in this, please feel free to donate to: D8WrK1jsFy9zpFwFZStaDTmX32pMZVdwXTm5rt9LsRKBQrz

KSM/DOT Enthusiast

My personal findings, thoughts, and rumor shares on Polkadot

0 comments